%20(1).jpg)

Key Takeaways

- Cryptocurrency losses can be used to offset capital gains and reduce your tax bill.

- If you sell and re-purchase an asset solely for tax purposes, your loss may be disallowed as a wash sale.

- Starting January 1, 2027, Australia's adoption of the Crypto-Asset Reporting Framework (CARF) will give the ATO direct visibility into transactions on overseas crypto exchanges.

Are crypto losses tax deductible?

In Australia, losses from cryptocurrency can be used to offset capital gains from crypto, stocks, and other forms of property.

If you have a net loss for the year, you can carry your loss forward to offset capital gains in future tax years.

What is tax-loss selling?

Because of the tax benefits, many investors choose to intentionally sell their cryptocurrency and other assets at a loss. This strategy is known as 'tax-loss harvesting' or 'tax-loss selling'.

Can I carry forward my crypto losses?

If you have a net loss for the year, you can carry your losses forward to offset gains in future tax years.

While there’s no limit to how many years you can carry your losses forward, you are required to use them to offset gains at the earliest available opportunity.

Can I carry back my crypto losses?

In Australia, you are not allowed to carry back crypto losses to previous tax years.

Are there any limits to crypto tax loss harvesting in Australia?

The Australian Taxation Office (ATO) actively enforces against 'wash sales,' the practice of selling an asset, claiming a capital loss, and then acquiring the same asset or a substantially similar one solely to gain a tax benefit.

Unlike the U.S., where a 30-day window between selling and re-buying an asset defines a 'wash sale,' the ATO doesn't set any specific timeframe. Instead, Australian tax law focuses on intent. A crypto transaction may be considered a wash sale if you sell a cryptocurrency at a loss and repurchase the same or a substantially identical asset soon after, with no genuine change in your financial position.

How does the ATO detect wash sales?

The ATO uses blockchain analytics and data-matching programs to identify wash sales. It receives transaction data from share registries and crypto-asset exchanges, including overseas platforms, not just Australian ones. Where the ATO's system identifies a wash sale, the capital loss claim is rejected.

The ATO can also apply Part IVA, the general anti-avoidance provision in Australian tax law, to schemes whose dominant purpose is obtaining a tax benefit.

What are the penalties for a wash sale?

If the ATO finds you've engaged in a wash sale, the consequences include:

- The capital loss claim in your tax return is denied

- Penalties of 25% to 75% of the tax shortfall

- Interest charges on top of the unpaid tax

- Possible further compliance action

If you realize you've made a mistake, voluntarily disclosing it to the ATO can significantly reduce penalties, often to 5% to 10% of the shortfall.

Can I use crypto losses to offset my income?

Individuals cannot use crypto losses to offset regular income (you can only offset other capital gains). However, businesses can treat crypto losses as a deductible expense.

What is the Crypto-Asset Reporting Framework (CARF)?

CARF is a new international tax transparency framework that gives tax authorities visibility into crypto transactions across borders. Australia committed to implementing CARF on February 9, 2026.

When does CARF take effect in Australia?

Legislation implementing CARF in Australia is expected during 2026, with a commencement date of January 1, 2027. The first reporting period will cover transactions from January 1, 2027 onward.

What CARF means for Australian crypto investors

Once CARF takes effect, Australian and overseas crypto exchanges will be required to report user transaction details to the ATO. The ATO will then share that information with tax authorities in other CARF-participating countries.

In short: starting January 2027, the ATO will receive direct transaction reports from crypto exchanges, including overseas platforms. Accurate reporting of capital gains and losses will be more important than ever.

For more information, see the Australian Treasury's CARF consultation page.

How do I claim crypto losses on my taxes?

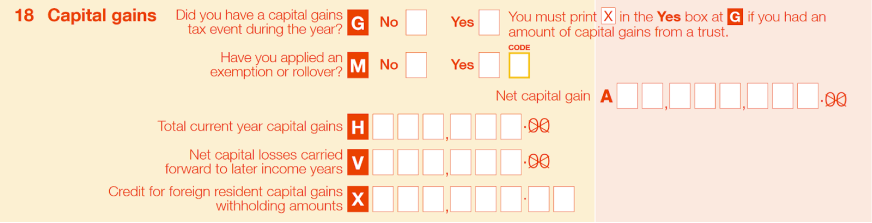

You should use the Capital Gain or Capital Loss Worksheet to calculate your net gain/loss for the year.

If you end the year with an overall net capital gain (after subtracting your capital losses from your capital gains), report this amount on H item 18 of your tax return.

If you instead have an overall net capital loss for the year, leave the net capital gain section blank and report your net capital loss on V item 18.

For the 2025-2026 tax year (which ended June 30, 2026), self-lodging individuals must submit their tax return by October 31, 2026. If you use a registered tax agent, the deadline is later.

How is cryptocurrency taxed in Australia?

Before we discuss how crypto losses can reduce your tax bill, let’s review the basics of cryptocurrency taxation.

In Australia, cryptocurrency is subject to capital gains tax and ordinary income tax.

When you dispose of cryptocurrency, you incur a capital gain or loss depending on how the price of your crypto has changed since you originally received it.

When you earn cryptocurrency, you’ll recognize ordinary income based on the fair market value of your crypto at the time of receipt.

For more information, check out our complete guide to how cryptocurrency is taxed in Australia.

How CoinLedger can help

Trying to keep track of your cryptocurrency gains and losses manually can be difficult. CoinLedger can help.

CoinLedger automatically connects with exchanges like CoinSpot and blockchains like Ethereum, so you can generate a comprehensive tax report in minutes. More than 700,000 investors around the globe use CoinLedger to simplify the tax reporting process.

Frequently asked questions

- Do you pay taxes on crypto losses?

- How much crypto losses can you claim?

- Does tax-loss selling apply to crypto?

- How long can capital losses be carried forward?

- How do I avoid crypto taxes in Australia?

- Do you pay tax on crypto only when you cash out?

- Will the ATO know if I do a wash sale?

- Does CARF affect how I claim crypto losses in Australia?

.png)

How we reviewed this article

All CoinLedger articles go through a rigorous review process before publication. Learn more about the CoinLedger Editorial Process.

CoinLedger has strict sourcing guidelines for our content. Our content is based on direct interviews with tax experts, guidance from tax agencies, and articles from reputable news outlets.