.jpg)

Key takeaways

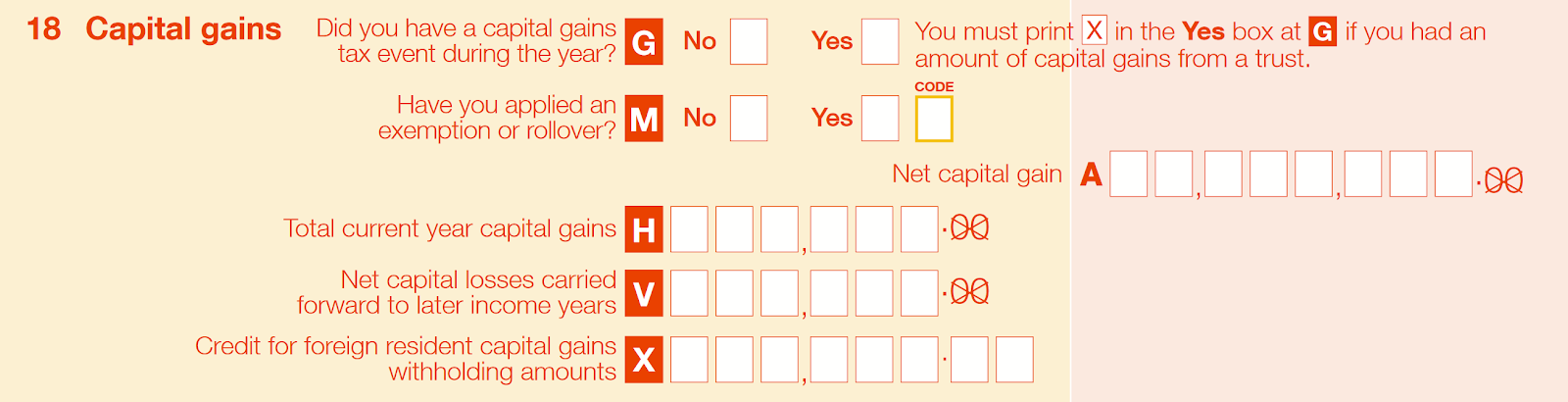

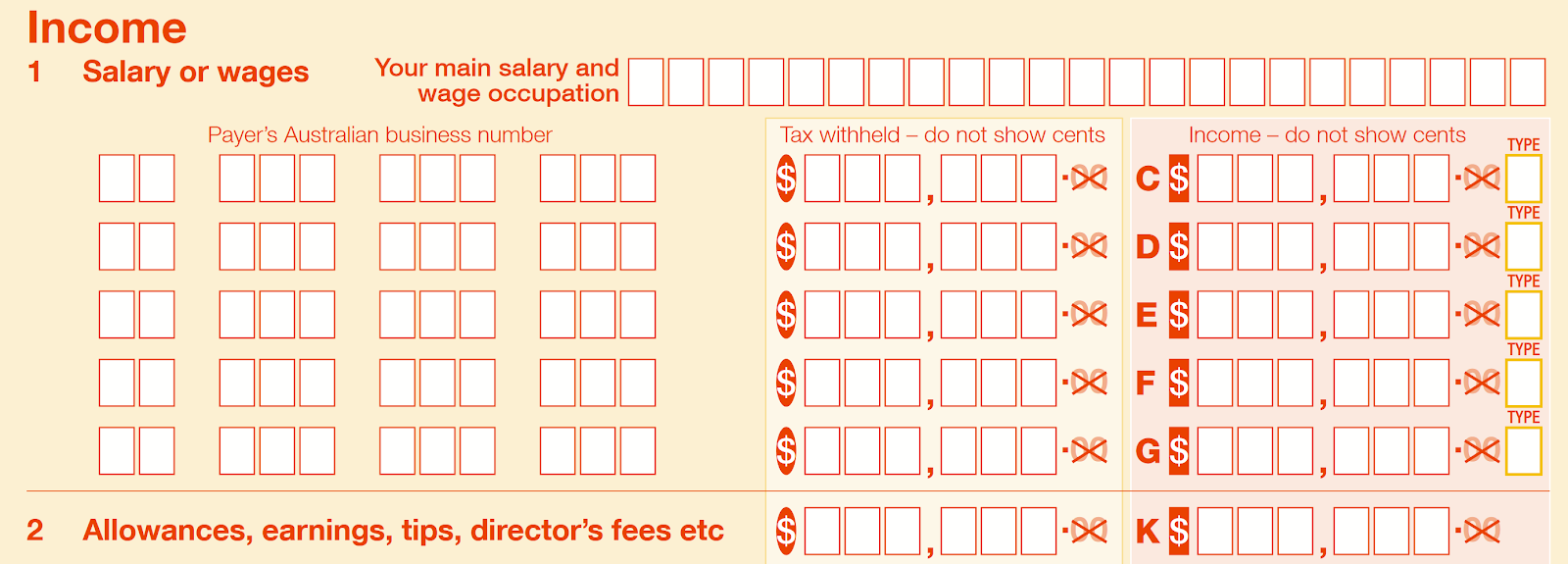

- Your CoinLedger capital gains report goes on Question 18 of the supplementary tax return; your income report goes on Question 2 of the individual return.

- The 50% CGT discount applies to crypto held 12 months or longer and remains in effect for the 2025-26 financial year, though it is proposed to be replaced with an inflation-adjusted discount from 1 July 2027.

- The ATO's crypto data-matching program covers up to 1.2 million Australians per year, so your reported figures should reconcile to your exchange data.

So you finished running your cryptocurrency tax reports within CoinLedger. Nice work. In this article, we walk through exactly how to use those reports to lodge your capital gains and income with the ATO.

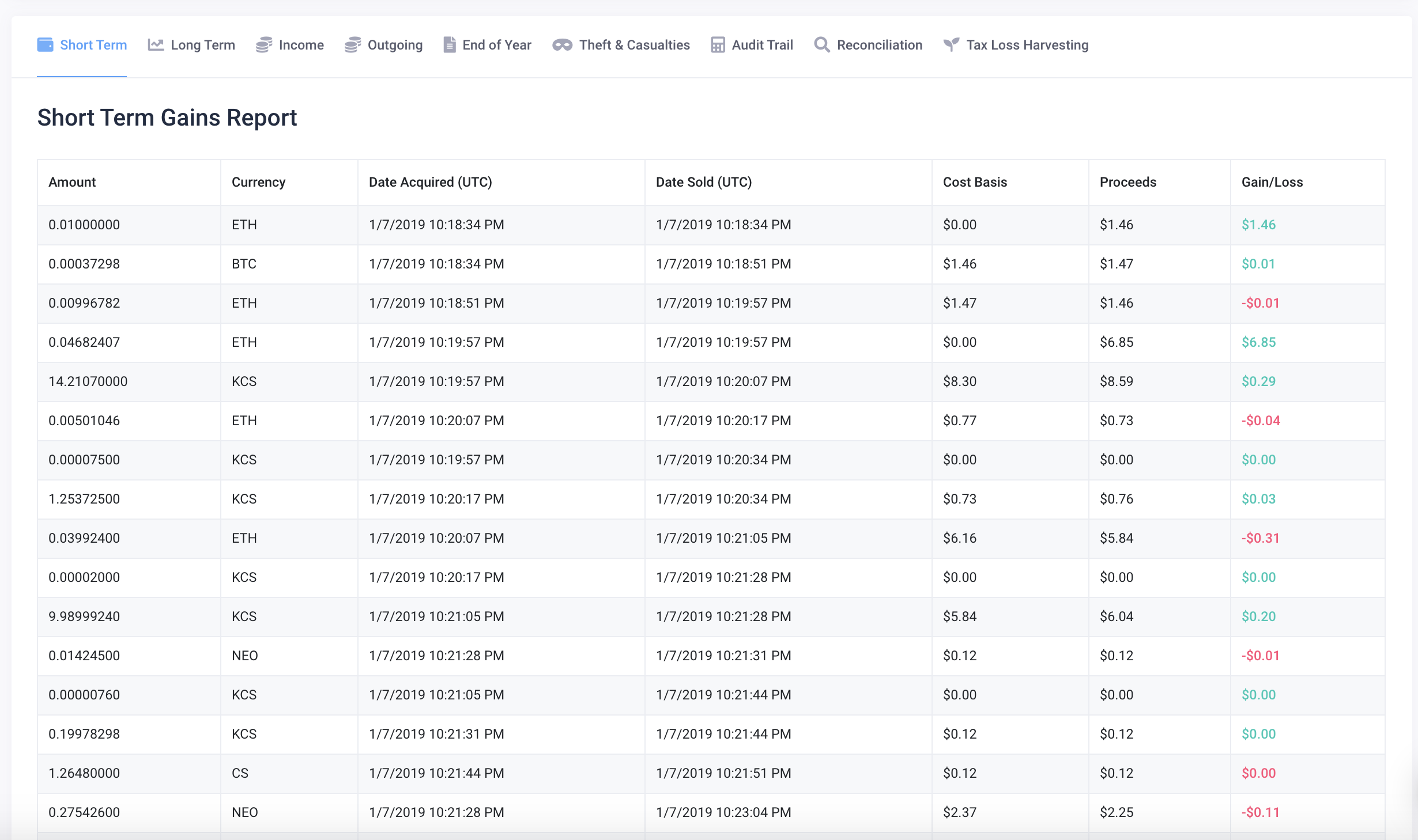

Capital gains and losses reports

Your capital gains and losses are separated by short term or long term. Short term gains and losses are on assets held and disposed of in less than 12 months. Long term gains are on cryptocurrencies held for longer than 12 months.

Long term capital gains qualify for the capital gains tax discount within Australia. The discount is 50% for individuals and trusts, and 33.33% for complying super funds and eligible life insurance companies. Learn more in our Complete Australia Crypto Tax Guide.

Heads up: the 2026-27 federal budget proposes replacing the 50% long-term CGT discount with an inflation-based discount, with a minimum 30% effective tax on long-term gains, from 1 July 2027. As of May 2026 this is still a proposal; the 50% discount remains in effect for the 2025-26 financial year. Watch for ATO confirmation before relying on the current rate beyond that window.

You can download these reports for yourself or send them to your accountant by clicking the "Downloads" or "Invite My Tax Professional" tab.

Your net capital gain is reported under Question 18 of the supplementary tax return.

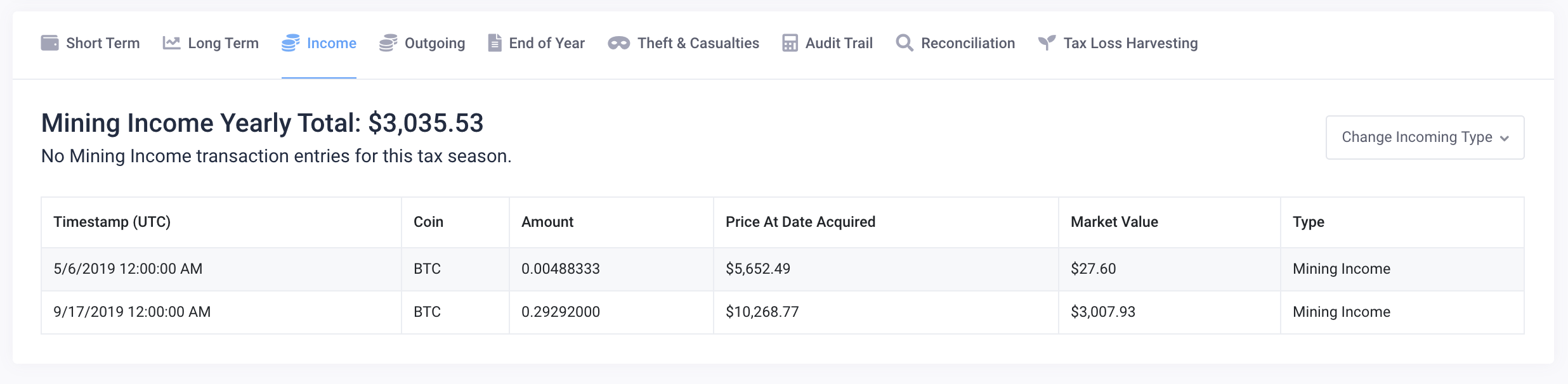

Income report

Any cryptocurrency-related income you recognise during the year, whether from mining, staking, or otherwise earning crypto, is reported in the matching Australian dollar amounts on your CoinLedger income report.

Navigate to the "Downloads" button within CoinLedger to download your complete income report. Use it to file your income yourself or hand it to your tax professional.

Crypto income belongs on Question 2 of the individual tax return (NAT 2541). That's where you report earnings that aren't salary or wages subject to standard withholding, such as tips and other income.

ATO data matching and what it means for your reporting

The ATO runs a crypto assets data-matching program that covers the 2014-15 through 2025-26 financial years. The program is expected to ingest data on between 700,000 and 1.2 million Australians each financial year.

The data comes from designated service providers — Australian crypto exchanges, plus a growing list of wallet and payment providers — and includes transaction-level history, account information, and personal identifiers.

For you, the practical implication is straightforward: the ATO can match the figures you lodge against what your exchange reported. If the two don't reconcile, the discrepancy is flagged for review. Lodge from your CoinLedger reports and keep your exchange downloads handy in case a follow-up question lands.

What CARF means for crypto reporting in Australia

In December 2025, the Australian government committed to implementing the OECD Crypto-Asset Reporting Framework alongside a parallel domestic transparency regime. Legislation is expected to be introduced during 2026, with a commencement date of 1 January 2027.

Once CARF is live, the ATO will automatically receive transaction-level data on Australian residents from foreign crypto exchanges, and Australian exchanges will share data on non-residents with their home tax authorities. Australia's first international CARF exchange is expected in 2028.

The practical implication: if you've used an offshore exchange, assume the ATO will see those transactions. Self-report now rather than waiting for the data flow to catch up.

Australian tax deadline

The Australian tax year runs from 1 July to 30 June the following year. If you are completing your tax return for the 2025-26 financial year (1 July 2025 – 30 June 2026), it is due by 31 October 2026 when self-lodged, or by 15 May 2027 when filed through a registered tax agent.

How to calculate your Australia crypto taxes in minutes

Looking for an easy way to file your Australian crypto taxes? Try CoinLedger, the crypto tax software trusted by 700,000 investors worldwide. With CoinLedger, you can import your transactions from hundreds of exchanges and blockchains, generate ATO-ready tax reports, and lodge with confidence — all in minutes.

Frequently asked questions

- Where do I report crypto income on my Australian tax return?

- Where do I report crypto capital gains on my Australian tax return?

- What is the 50% CGT discount and how do I claim it?

- What's the deadline for lodging my 2025-26 crypto tax return?

- Does the ATO know about my crypto?

- Do I need to report crypto if I didn't sell?

.png)

How we reviewed this article

All CoinLedger articles go through a rigorous review process before publication. Learn more about the CoinLedger Editorial Process.

CoinLedger has strict sourcing guidelines for our content. Our content is based on direct interviews with tax experts, guidance from tax agencies, and articles from reputable news outlets.